The Global Uptick in Electric Vehicle Batteries and Africa’s Strategic Role

Africa stands at a crossroads as the global shift toward electric mobility unfolds. The continent has vast minerals crucial for the production of electric vehicle batteries. However, as battery technologies and international supply chains evolve, Africa must adapt to maximise the value of its resources.

This article examines how African countries can benefit from the growing battery market, driven by the increasing demand for electric vehicles. It begins by looking at changing battery technology. It then delves into smart policies informed by global best practices, such as the EU’s framework. Finally, we tackle ways to add local value, manage end-of-life electric vehicle batteries, and boost regional cooperation.

The future for Africa’s mineral prosperity calls for a bold step in leveraging mineral resources, investing in local manufacturing, and aligning with initiatives like AfCFTA. This move will unlock the potential to meet global demand, accelerate development, and increase energy access by contributing to the electric vehicle battery supply chain.

Africa’s Role in the Rising Demand for Electric Vehicle Batteries

The global demand for batteries, particularly for electric vehicles (EVs), is surging as the world transitions to zero-emission transport solutions. According to BloombergNEF, lithium-ion battery demand for electric vehicles (EVs) is expected to increase from approximately 700 GWh in 2023 to over 3,500 GWh by 2030, driven by global EV adoption (BloombergNEF Electric Vehicle Outlook 2024) at a compound annual growth rate (CAGR) of approximately 25%.

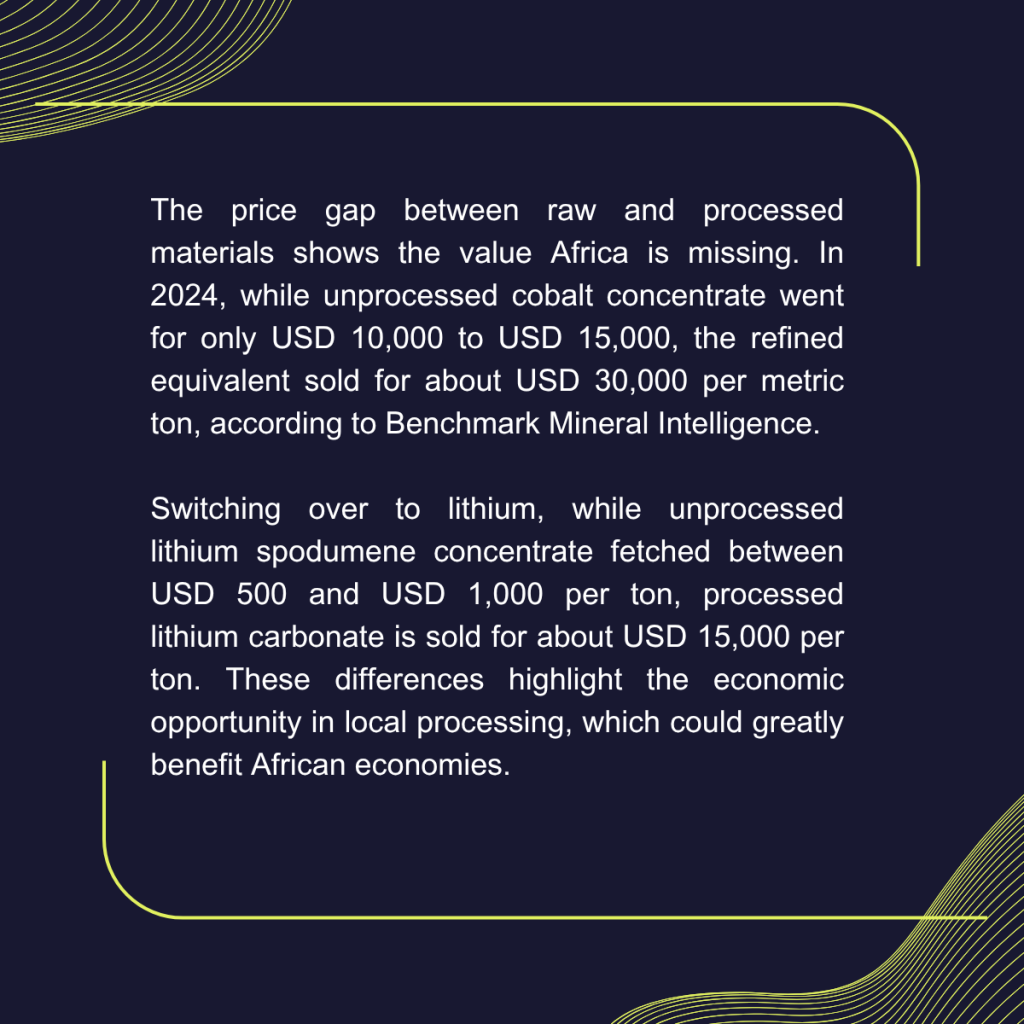

Africa plays a key role in the electric vehicle battery supply chain, primarily by providing raw materials. The Democratic Republic of the Congo (DRC) produces over 70% of the world’s cobalt, according to the U.S. Geological Survey (USGS), making it a key contributor to global lithium-ion electric vehicle battery production.

Additionally, countries like Zimbabwe, with Africa’s largest reserves of lithium, at 480,000 metric tons, and Nigeria with high-grade lithium of between 1-13%, multiple folds above the standard minimum exploration concentration of 0.4%, have strong potential to add value and deepen Africa’s role in the electric vehicle battery industry. However, African countries still export most minerals in their raw form, missing out on value-added opportunities that come from processing and manufacturing.

(Benchmark Mineral Intelligence Cobalt Price Assessments).

The Shift in Electric Vehicle Battery Chemistries and Implications for Africa

The global electric vehicle battery market is undergoing rapid change. There is a shift from using traditional cobalt and nickel-based batteries to materials such as lithium-iron-phosphate (LFP) and sodium-ion (Na-ion) batteries. This change is occurring due to lower costs, improved performance, and access to local raw materials.

LFP Batteries

Lithium-ion phosphate (LFP) batteries held just under 30% of the market share in 2022, primarily due to their adoption by Chinese original equipment manufacturers (OEMs) such as BYD and Tesla. They are preferred for their durability, lower cost, and reduced reliance on critical minerals like cobalt and nickel, as they utilise iron and phosphorus instead.

Over 95% of heavy-duty electric trucks in China utilise LFP cathode chemistries, driven by their suitability for high mileage and cost-sensitive buyers, given that more than 50% of truck purchases in the country are made on credit or lease.

Sodium-Ion Batteries

Sodium-ion batteries are a promising new option. They cost about 20–30% less than LFP batteries and don’t use lithium, helping avoid price swings and supply issues.

Their energy density ranges from 100 to 160 Wh/kg, comparable to that of LFP batteries, which can reach up to 186 Wh/kg. This makes sodium-ion batteries a suitable choice for applications such as urban vehicles and stationary energy storage systems.

Sodium-ion batteries can be transported at 0 volts, making them a safer option compared to lithium batteries. As of 2024, over 100 GWh of sodium-ion battery production is already running or announced, mainly in China. This total compares to a global battery manufacturing capacity of 1,500 GWh, according to a 2024 research paper.

Implications of Using New Electric Vehicle Batteries in Africa

For African countries, which are major suppliers of cobalt and nickel, the shift towards LFP and sodium-ion batteries poses both challenges and opportunities. The reduced demand for cobalt could impact export revenues, particularly for the Democratic Republic of the Congo (DRC), which accounts for over 70% of global cobalt production.

However, Africa’s significant lithium reserves, located in countries such as Zimbabwe and Nigeria, remain crucial for producing LFP batteries. To capitalise on this, African nations must invest in local processing and manufacturing capabilities to add value to their mineral resources rather than exporting them in raw form. Moreover, developing sodium-ion batteries could open new avenues for Africa to leverage its other mineral resources or develop alternative supply chains.

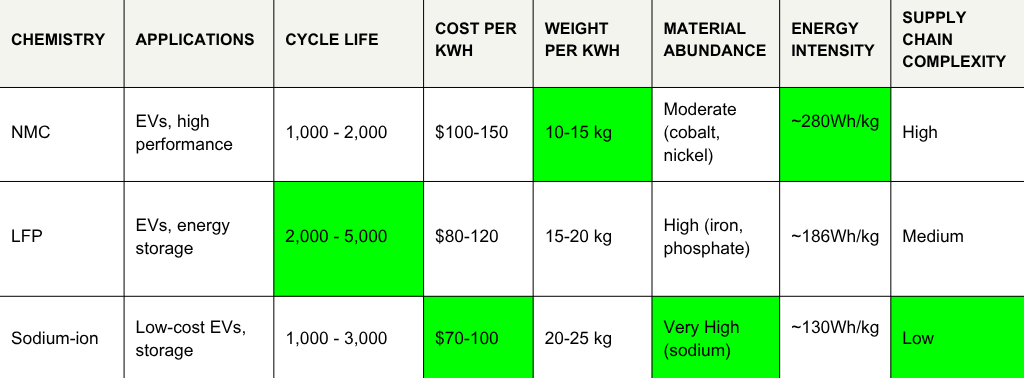

Comparative Analysis of Electric Vehicle Battery Chemistries

To provide context, here’s a tabulated comparison of different electric vehicle battery chemistries. Focus is on NMC, LFP, and sodium-ion batteries.

Source: Battery Design

Global and African Electric Vehicle Policies

Global commitments to phase out internal combustion engine (ICE) vehicles are accelerating the demand for electric vehicle (EV) batteries. In Africa, Ethiopia became the first country globally to ban the imports of ICE vehicles, effective January 2024. Meanwhile, in Rwanda, starting in January 2025, only electric motorcycles will be eligible to acquire new moto-taxi operating licenses and registration. The European Union (EU) is also committed to operationalising a ban on new ICE vehicle sales by 2035.

The EU’s Battery Regulation (EU) 2023/1542, effective August 2023, provides a robust framework for managing batteries that African countries can learn from and adapt to.

Key Provisions of the EU Battery Regulation

The EU Battery Regulation, adopted on 28 July 2023, aims to ensure sustainability, safety, and circularity throughout the entire battery lifecycle. It aims for a 14-fold increase in global demand by 2030, with the EU expected to account for 17% of this growth. Important highlights include:

- Sustainability Criteria: Batteries must meet carbon footprint thresholds. EV batteries must submit declarations by February 18, 2025, and industrial batteries (with a capacity greater than 2 kWh) must submit declarations by February 18, 2026. By 2030, batteries must contain a minimum of recycled content, including 12% cobalt, 4% lithium, 4% nickel, and 85% lead, which is expected to reduce reliance on virgin materials by an estimated 20%.

- Labelling and Transparency: By August 18, 2026, all batteries must display labels with the manufacturer’s date, weight, and chemical composition. A digital battery passport, mandatory for electric vehicles (EVs), light means of transport (LMT), and industrial batteries (greater than 2 kWh) by February 18, 2027, will provide data via QR codes, enhancing transparency for 100% of in-scope batteries.

- Waste Management: Collection targets aim for 65% of portable batteries to be recycled by 2025 and 70% by 2030, with recycling efficiency targets of 80% for nickel-cadmium batteries and 50% for other types of waste batteries by December 31, 2025. Material recovery targets for cobalt, copper, lead, lithium, and nickel take effect on December 31, 2027, to recover 90% of these materials by 2030.

- Battery Categories: The regulation defines five categories

- Portable batteries

- Light means of transport (LMT) batteries

- Starting, lighting and ignition (SLI) batteries

- Industrial batteries

- Electric vehicle (EV) batteries

- Conformity and Surveillance: All batteries require CE marking from August 18, 2024, with notified bodies involved for EV, LMT, and industrial batteries (>2 kWh), affecting 1.5 million batteries annually

Timelines

The regulation’s phased implementation began on February 18, 2024, with initial provisions including:

- CE conformity assessments for all batteries, ensuring compliance with safety and environmental standards.

- Restrictions on hazardous substances (e.g., mercury ≤ 0.0005%, cadmium ≤ 0.002% in portable batteries) apply to 100% of batteries sold in the EU

Major provisions applying from August 18, 2024, include:

- Safety requirements for stationary battery energy storage systems, which affect 90% of large-scale storage applications.

- Performance and durability documentation for EV, LMT, and industrial batteries (>2 kWh), covering approximately 70% of the EU’s industrial battery market.

Significant provisions delayed until 2032 include:

- Maximum Carbon Footprint Thresholds (August 18, 2031): Batteries must comply with upper limits on lifecycle carbon emissions, likely delayed to allow manufacturers time to develop low-carbon production processes, given the complexity of retooling supply chains for an estimated 50% reduction in emissions

- Recycled Content Targets for LMT Batteries (August 18, 2033): LMT batteries must meet recycled content thresholds, delayed due to the smaller scale of LMT battery production and the need for recycling infrastructure development, which currently handles only 10% of LMT batteries These delays likely stem from the need for technological advancements and infrastructure scaling to meet stringent requirements across diverse battery types.

Repeal of the 2006 Battery Directive

The 2006 Battery Directive (2006/66/EC) will be repealed on 18 August 2025, with a select number of provisions remaining in effect for a limited period. Alongside the repeal, three significant changes will occur:

- Introduction of Supply Chain Due Diligence (August 18, 2025): Companies with a turnover exceeding €40 million are required to implement due diligence policies for cobalt, lithium, nickel, and graphite, affecting approximately 80% of battery producers. This ensures ethical sourcing, with third-party verification impacting an estimated 500,000 supply chain audits annually (EU Batteries Regulation: Next implementation stage aims at greater transparency | Herbert Smith Freehills).

- Enhanced Extended Producer Responsibility (EPR): Updated EPR requirements mandate producers to finance collection and recycling, with new targets (e.g., 65% collection for portable batteries by 2025), increasing recycling rates by 15% compared to the 2006 Directive (Understanding EU Battery Regulation | 2023/1542 – Acquis Compliance).

- Mandatory Waste Battery Management: Producers must establish take-back and collection systems, ensuring 100% of waste batteries are treated per regulation standards, a significant shift from the 2006 Directive’s less stringent requirements, which achieved only 45% collection rates (EU New Battery Regulation focuses on sustainability, waste management and due diligence | Norton Rose Fulbright).

Strategies for African Countries to Capture Value from Electric Vehicle Batteries

Africa’s abundant mineral resources and the booming electric vehicle (EV) battery market—set to grow from 700 GWh in 2023 to 3,500 GWh by 2030—leverage regional frameworks, enabling African nations to transition from raw material exporters to global leaders in the battery value chain. The following three strategies can be considered to transform its future:

Progressive Regulations for Local Value Capture, Paired with Incentives and R&D

Picture Africa not just exporting raw cobalt and lithium, but manufacturing batteries for the global market. Regulations mandating an increase in local content in battery production, paired with incentives and robust R&D, can make this a reality. The value gap between unprocessed and processed minerals ranges from 3 to 15 times, making it too lucrative to forego. By 2030, integrating mining and refining could achieve 35–40% cost competitiveness. Countries like Morocco and Tanzania are well-positioned to produce cost-competitive lithium-iron-phosphate (LFP) batteries, but success depends on the development of local R&D hubs to build expertise. South Africa’s Solar MD, which combines imported cells with proprietary systems, shows the power of homegrown innovation. Tax breaks, subsidies, and R&D grants can attract private investment; however, Africa must avoid over-reliance on foreign technology, a trap that has been seen in some Asian markets. Establishing local innovation hubs is crucial for building self-sufficiency, ensuring Africa not only participates but also leads in the global battery revolution.

Leveraging Regional Trade and Political Alliances for Efficiency and Scale

What if African countries collaborated like the EU to create a battery market powerhouse? The African Continental Free Trade Area (AfCFTA) and Regional Economic Communities (RECs), such as ECOWAS, EAC, and SADC, is aimed at connecting 1.3 billion people and tapping into a $3.4 trillion GDP, a clear opportunity for the battery value chain to ride on it. The potential DRC-Zambia battery plant, sourcing materials regionally, could be a clear demonstration of how collaboration enhances efficiency and attracts global investment. Building on ECOWAS’s vehicle emission regulations, RECs can standardise battery inspection, assembly and progressive manufacturing, allowing for added localised value creation. This collective approach, mirroring the EU’s economic bloc, enables Africa to pool its resources, share best practices, and negotiate more favourable terms with global partners. However, smaller economies risk marginalisation, as seen in some global trade blocs. Coordinated resource mobilisation, such as joint financing for production facilities, can ensure equitable benefits across nations, positioning Africa as a formidable player in the global battery value chain.

Capitalising on Downstream Opportunities Through Repair, Repurposing, and Recycling

Every African country, regardless of upstream capabilities, can transform battery waste into economic opportunity through repair, repurposing, and recycling. As EV adoption accelerates, end-of-life batteries are expected to surge, offering both economic and environmental benefits. Repurposed batteries can stabilise grids or power off-grid communities, addressing energy access for 600 million Africans. Recycling recovers valuable materials, such as cobalt and lithium, thereby reducing reliance on virgin mining. South Africa’s Cwenga Lib and Nigeria’s planned recycling plants showcase modular, efficient facilities. The EU’s Battery Regulation, aiming for 90% material recovery by 2030, provides a blueprint for Africa to develop robust waste management policies. The pitfall to avoid is informal recycling, which has caused lead poisoning in Nigeria and Senegal. Formalised systems, supported by regional cooperation, can create jobs, prevent environmental dumping, and position Africa as a leader in the circular battery economy.