In Summary

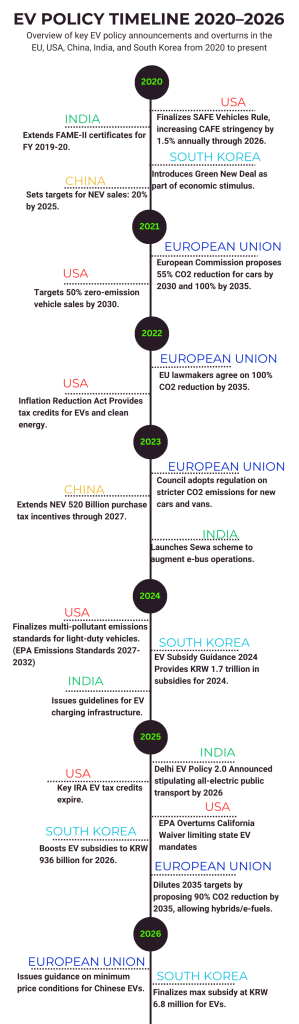

- In Dec 2025, the EU slowed progress on the Automotive Package, reducing the 2035 target from 100% to 90% CO₂ reduction and allowing hybrids and e-fuels.

- Asia continues to accelerate with China (+28%), India (+16%), South Korea (+50%) YoY EV growth in 2025, driven by consistent/strengthened policies

- Africa outperforms the global slowdown, with 30–35k active EVs, segment growth of 28–44% YoY (well above the global 20%), and is driven by commercial/public fleets.

- The opportunity is in the gap. EU hesitation creates a short-term dip in mineral demand but allows Africa to pursue pragmatic, affordable electrification and local value chains without mismatched timelines.

- Africa must act now. Unite around a clear, time-bound e-mobility vision (2035–2050–2063), prioritise technology sovereignty, mineral beneficiation, AfCFTA-enabled assembly, and rapid electrification of high-growth shared/commercial segments—no legacy baggage is an advantage.

At a time of heightened global geopolitical tensions, from America’s shortsighted tariff wars on protecting its market, to Europe’s trilemma; Greenland’s looming future, Russia-Ukraine conflict and the resulting energy crisis, to the recent watering down of its ambitious 2035 auto emissions reduction, the resulting market signals, including those to Africa, are confusing and opportune at the same time. The continent and its individual states can no longer afford to stand by as global developments unfold, but must define and pursue their continental and global interests.

So what just happened with the EU’s commitments?

In December 2025, the EU introduced the Automotive Package, a raft of measures to support the sector’s transition. Notably, the Union revised its 2035 ambition to achieve a 90% reduction in auto tailpipe emissions, down from 100%. The remaining 10% will be covered using low-carbon steel or alternative fuels such as biofuels. Other supporting measures accompanying the targets include a EUR 1.8 B battery booster to strengthen EU battery value chains, automotive omnibuses, and mandatory state-level targets for corporate fleets.

Despite the comprehensive support, the step back on ambition reflects the level of readiness (or lack thereof) of the Union’s industry to compete with other global players, such as China, India, South Korea and the USA.

It’s happened before, and will continue

The announcement came just 3 short years after the initial target was set in 2023. This delay isn’t the first or the last in this global leadership race. In 2023, the UK postponed its ICE sales ban from 2030 to 2035. The USA’s initial Inflation Reduction Act (IRA) of 2023 (expired in 2025), and Biden’s 2021 executive order aiming for 50% zero-emission vehicle sales by 2030, have since been shelved, with only a handful of states (through the Advanced Clean Cars II rules) pursuing isolated initiatives to promote adoption.

The rest of the world is charging ahead

China, South Korea, and India, on the other hand, are standout economies that have maintained, and even advanced, their commitments not only to their maturing domestic markets but also to their growing global exports. Actions ranging from China’s 2020 NEV Industry Development Plan (targets surpassed), to South Korea’s 2020 Green New Deal (targets surpassed), to India’s FAME I&II initiatives and Delhi’s proposed EV Policy 2.0, which will eliminate ICE two-wheeler registrations from 2026, are all clear signs that the EV momentum is not slowing down anytime soon.

Zooming Out: The global demand follows strong policy

2025 global EV sales reached 20.7 million units, marking 20% YoY growth, a slowdown from previous years, mainly driven by low demand from leading markets in Europe and the USA, which represent 30-40% of global EV sales.

Africa’s 2025 EV stock growth showed between 20-44% growth, outpacing the global average, and accounting for just under 0.2% of EV fleets globally. India hit 16% YoY growth, China 28%, while South Korea hit 50% YoY growth in 2025 data.

The writing is on the wall: EV demand is surging in markets that continue to strengthen their policies, including Africa, and cooling in markets that are weakening theirs. There is a clear opportunity for Africa to double down on its industrialisation strategy in the minerals and automotive value chains, leveraging regional cooperation, including the continental free trade area (AfCFTA).

What are the three standout messages for Africa’s future as a result of the EU’s announcement?

Message 1: Introduce Africa’s E-Mobility Vision

At this rate of global change, Africa’s future without a clear vision will remain only a bargaining chip for global powers. The continent, economic communities and individual states need to be coalesced around a clearly articulated vision. This vision should be time-bound and relevant: first to the near term (2035), then to the medium term, targeting global carbon neutrality (2045-2050), and, in the long run, aligned with the continental vision 2063. It should also recognise the continent’s high-growth areas in public, shared, and commercial vehicles. It should press for industrialisation of its minerals and its finished products to discourage long-term imports of fully built units. The vision should clearly outline Africa’s just energy transition, leveraging both renewable and non-renewable resources to enhance global competitiveness while maintaining climate leadership.

Message 2: Embrace Technology Independence

The EU’s Battery Booster is a clear signal of its commitment to reinforcing domestic value chains and upholding production sovereignty. Africa, with its vast mineral resources, risks remaining an exporter of raw materials, experiencing short-term demand drops as the EU’s EV demand declines, and, in the long run, missing out on technology transfer if its regulatory framework remains lax. The call to action is for policymakers and industry innovators to emphasise increasing local production and to explore diversification strategies to meet local and global demand.

As the continent’s fleet is projected to grow 4-5 times by 2050, with used-vehicle imports accounting for an 80% share, the future remains uncertain unless local policy realities improve toward a clear electrification path with increasing local value addition.

Electric mobility in Africa is a booming industry. The 30,000-unit vehicle market has been proven ripe for public, shared, and commercial vehicles, growing up to 24% faster than the global average. These segments are also procuring brand-new vehicles from the start. By directly championing the electrification of these vehicle segments through matching policy and investment mobilisation, the market signal changes from one of waiting to one of inviting aligned partners.

No Legacy? No Problem

African countries, apart from South Africa, Morocco, and Egypt, have no legacy strings that underpin their speed in adopting electric vehicle manufacturing and assembly. This lack allows countries to attract new automotive investments, with a focus on electric vehicles for high-growth segments of public, shared, and commercial vehicles.

Regional Economic Communities such as EAC, ECOWAS, and SADC are prime infrastructure platforms to leverage in establishing assembly and manufacturing facilities in the new era of reduced component requirements for EVs compared to ICE vehicles.

Conclusion

Current global developments signal an evolving landscape of priorities as countries and regions balance self-sufficiency and technological advancement amid volatile security concerns. African countries are at a watershed moment, looking to one another for ways to collaborate on a clean automotive future. A clear, unifying ambition, coupled with the practical development of energy infrastructure and financial and human capital, will enable individual countries and regions to play an active role in shaping their own electric future.